Table of contents

Here’s the scene: the holiday season is just around the corner, and the customer rush is sending your warehouse into overdrive. Similarly, a local construction company needs materials for an upcoming job without much time to plan. In both cases, these businesses don’t have enough cash flow to meet growing demand and tap into their revenue potential. One possible solution? Short-term financing.

This type of financing is useful for businesses that need a quick cash infusion without the drawbacks of long-term interest. Short-term funding is an excellent option for covering new or unforeseen expenses, while working capital covers other operating costs.

In this article, we’ll examine the different types of short-term financing, their pros and cons, how they differ from long-term loans, and how a business can qualify for this type of funding.

What is Short-Term Financing?

Short-term financing is a business loan or line of credit structured so that payment is due much sooner than a traditional long-term loan – usually between six and 18 months. You’ll typically find short-term loan options available at banks, credit unions, or private credit lenders.

Once the loan is approved, the business will receive a lump sum deposited into its bank account. The payment frequency and amount will be pre-arranged as part of the loan terms. These short-term loans might appeal to businesses that want a quick influx of cash for equipment, more inventory, or urgent new hires.

Types of Short-Term Financing

Businesses can choose from many types of short-term loans. The financing option you’ll need will vary based on your specific situation, such as the purpose of the loan and how long you’re comfortable with the repayment terms. Here are three of the most common short-term financing examples:

Lines of Credit

A business line of credit works a lot like a credit card. The lender opens the line of credit, and you’ll have access whenever needed. Like any type of revolving debt, you can withdraw up to the credit limit and pay interest only on what you use. This financing option may make sense for disciplined business owners who want to stay in control of their business debt.

Cash Flow Financing

With cash flow financing, businesses can secure quick and easy capital by leveraging future sales. This alternative form of financing is typically unsecured – meaning you won’t need to put up unpaid invoices, equipment, or property as collateral. You also won’t have a strict monthly payment schedule, as you can make payments based on your daily sales and adjust them to fit the business’s performance.

Term Loans

Term loans are just that – loans expected to be repaid over a certain term. Small business loans usually run between six to 18 months, while longer-term loans – such as Small Business Advancement (SBA) loans – typically last anywhere from three to ten years. The purpose of the loan will help you determine the best repayment terms. For example, large equipment loans are usually a long-term solution.

Advantages and Disadvantages of Short-Term Financing

Any type of loan will have its share of pros and cons – and short-term financing isn’t any different. Let’s dig into some of the advantages and disadvantages of this type of financing.

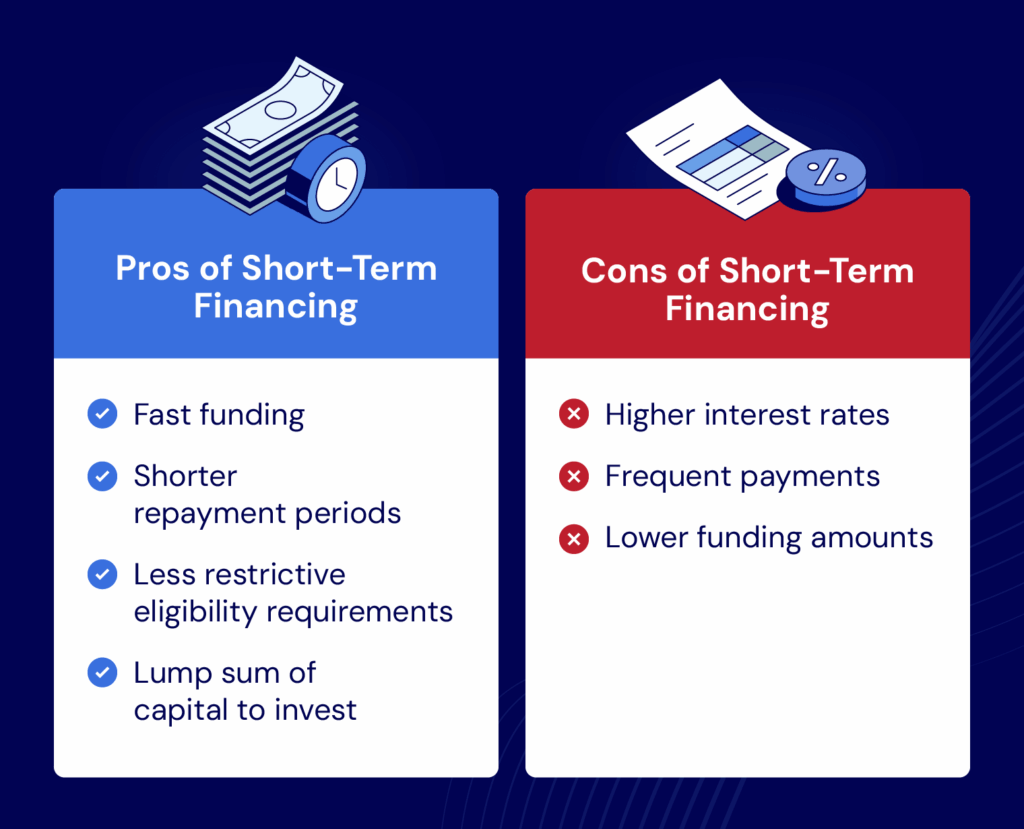

Advantages

There’s a lot to like about short-term financing because it has many benefits. Some of those advantages include:

- Fast funding: Some lenders can deposit funds into your account within 24 hours.

- Shorter repayment periods: Terms usually run between six to 18 months.

- Less restrictive eligibility requirements: These loans come with shorter terms and lower balances, so they are easier to qualify for.

Disadvantages

Despite several benefits, short-term financing doesn’t come without drawbacks. Some examples include:

- Higher interest rates: Short-term financing may come with higher interest rates with regulations varying by state and rules varying by lender.

- Frequent payments: The payment schedule is predetermined between you and the lender, but short-term loans typically require more frequent payments than traditional financing options.

- Lower funding amounts: This type of financing is ideal for a quick influx of cash but won’t make sense for businesses with larger budgets and more complex financing needs.

Differences Between Short-Term and Long-Term Loans

As you might expect, short-term and long-term loans have quite a few differences. Here’s what you can expect from each.

| Short-Term Loans | Long-Term Loans | |

|---|---|---|

| Term Length | 6-18 months | 2 to 10 years |

| Interest Rates | Variable/High | Variable/Low |

| Amounts | Lower (depends on business qualifications) | Higher (depends on business qualifications) |

| Eligibility | Less restrictive | More restrictive |

How to Qualify for a Short-Term Loan

Repayment length on short-term loans is fairly consistent, but the factors that play into qualifying for this financing option can vary greatly based on the lender. That said, many loan providers will look for similar markers to determine funding and term length before approving financing. Some eligibility requirements include:

- Business and personal credit score: As with any loan, the lender will look at credit scores to determine a business’s reliability when it comes to repayment.

- Time in business: If your business has been operating for a while, you’ll have a better chance of loan approval because this speaks to the viability of your company. Most lenders will require you to be in business for at least six months to qualify.

- Annual revenue: This gives a lender the best idea of your business’s performance, and with most lenders, you’ll need an annual revenue to support repayment. Some lenders might also require collateral – such as inventory financing.

Get Started Growing Your Business Today

Here at National Business Capital, we have plenty of loan options to help your business in the short or long term. Our expert business finance advisors would love to chat with you, answer questions, and guide you through every step of the loan process. Apply now to find the best short-term financing options for your business.

ABOUT THE AUTHOR

Joseph Camberato is the CEO & Founder of National Business Capital, where he has led the company in funding more than $3 billion for growth-minded businesses since 2007. With firsthand experience building NBC from a startup into a national private lender, Joe writes on the economic forces shaping access to capital, including interest rate shifts, private credit trends, and the challenges mid-sized companies face when banks pull back.