What’s the difference between a line of credit vs cash flow financing? Here’s a quick breakdown:

| feature | business line of credit | Cash Flow financing | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Type | Revolving credit | Lump sum funding | Typefeature: Type business line of credit: Revolving credit Cash Flow financing: Lump sum funding | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Payments | Weekly and monthly | Weekly and monthly | Paymentsfeature: Payments business line of credit: Weekly and monthly Cash Flow financing: Weekly and monthly | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Flexibility | Withdraw as needed | Fixed funding, flexible repayment | Flexibilityfeature: Flexibility business line of credit: Withdraw as needed Cash Flow financing: Fixed funding, flexible repayment | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cost | Interest only on outstanding amount | Flat cost, no prepayment penalties | Costfeature: Cost business line of credit: Interest only on outstanding amount Cash Flow financing: Flat cost, no prepayment penalties | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

A business credit line functions more like a credit card than other types of term loans, giving you ongoing access to capital.

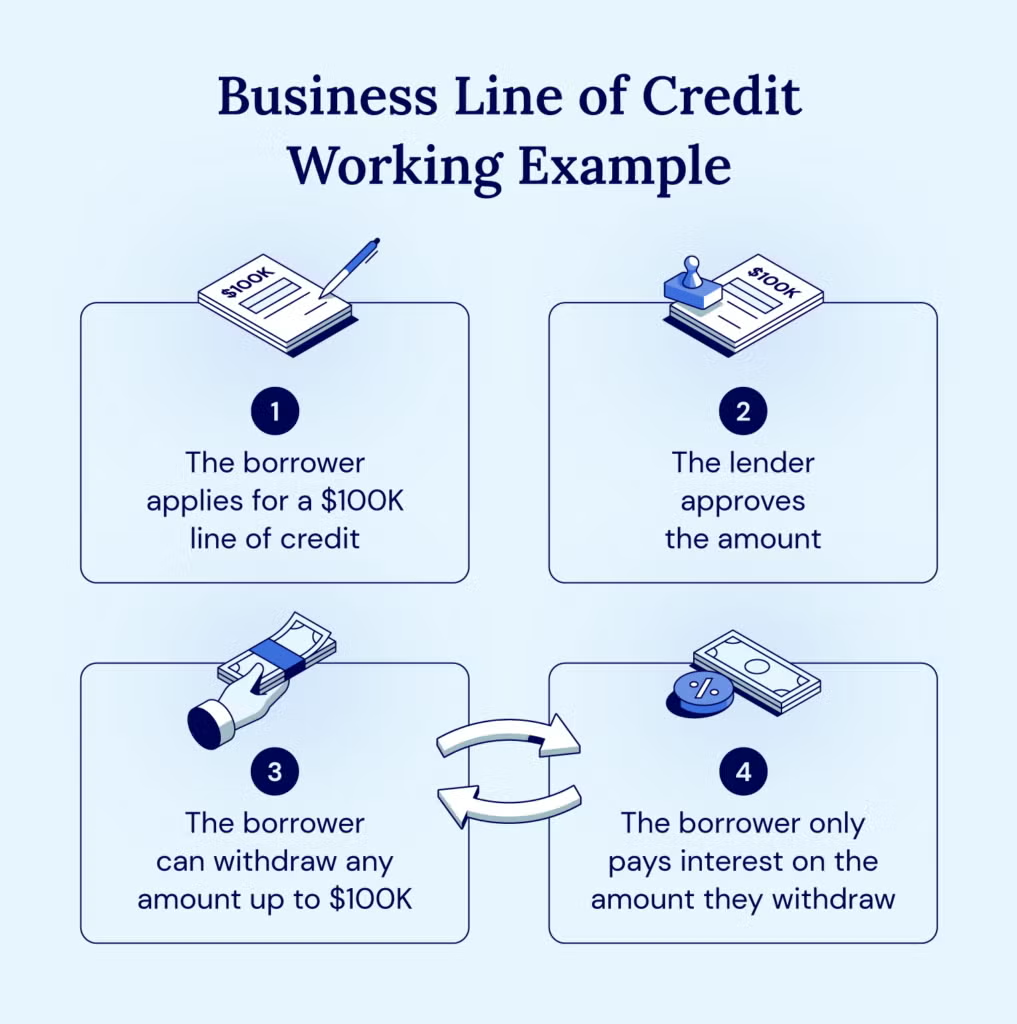

After qualifying, you’ll receive a total credit limit and can transfer any amount you need from your credit line to your business bank account for quick business funding.

Secure a credit line based on your business revenue.

Access funds anytime, in any amount.

Interest applies only to withdrawn funds.

Repay and access more capital as needed.

They took the time to help me find the right financing for my business. Extremely straightforward!

Funds as you need them, when you need them

Your performance and potential are how we determine if you’re a good fit for a business line of credit. Check these two boxes and you’re on track for approval.

- 1+ year in business

- $500,000+ in annual revenue

Not a match? Check out your other options

Have this information on hand and you’re all set.

- Business formation documents

- Bank statements (6 months)

- Business tax returns

- Financial statements

FAQs

A business line of credit is a type of loan that gives you flexible access to cash on an as-needed basis.Unlike a loan, it’s a revolving credit line—meaning you can withdraw funds as needed and only pay interest on what you use. More cash becomes available as you pay down your balance, keeping your business financially agile.

Business lines of credit are ideal for small business owners who want to keep ownership and control. They can be used for emergencies or any other business-related purpose.

Business lines of credit function more like credit cards than other types of term loans—but you can write off interest on lines of credit when tax season comes.

Once you qualify for a business line of credit, you’ll receive a total credit limit from which you can transfer any amount you need to your business bank account in any number of installments for quick business funding. A credit line puts you in control—use what you need, when you need it, with no obligation to draw the full amount.

You can continue to access additional cash as long as unpaid withdrawals stay under the credit limit. Instead of paying interest on the entire credit limit, you’ll only pay interest on what you take.

Before signing an agreement, ask for clear information about any fees tied to not using the credit line—such as non-utilization fees. Avoid any agreements that don’t offer clear, transparent terms.

| Remember: The best business line of credit is one that fits your business now and as it grows. It should match your cash flow, not restrict it. Use it to seize opportunities, manage gaps, or smooth out seasonal swings. Terms and flexibility vary widely between lenders offering business lines of credit—choose an experienced and trustworthy lender who can help you achieve your business’s goals and adapt as situations change. |

|---|

While the specific steps may vary by lender and credit type, the basic application process for a business line of credit follows this structure:

- Gather documentation.

- Submit applications for a few different business lines of credit lenders.

- Review and compare loan terms.

- Select your ideal option.

The documentation you typically need includes:

- Driver’s license

- Business bank statements (1 year)

- Business credit score & financial statements

- Proof of ownership (K1, schedule C, EIN, certificate of corporation, etc.)

- Business tax returns

- Collateral (if secured)

- Cash flow statement

- Business plan

Applying through National Business Capital can simplify this process — you can learn more about your options from our team of expert advisors with only one application.

Banks and credit unions often set the bar high, imposing rigid requirements and demanding qualifications that can shut out businesses with imperfect credit or limited financial histories.

But they’re far from your only option.

At National Business Capital, we prioritize your performance and potential, not just traditional metrics like history and credit. We make it faster and easier to qualify for a flexible business line of credit that fits your needs—because with the right partner, accessing capital becomes less complicated than you may expect.

Not at all, especially with small business lenders and private credit lenders like National Business Capital. While traditional banks have strict criteria, National Business Capital evaluates your business potential, cash flow, and revenue – helping you qualify faster.

Yes! LLCs, corporations, and partnerships can all qualify for a business line of credit.

A $250,000 credit line means you can borrow any amount up to your limit. Withdraw $250,000? You only pay interest on that, nothing more.

A business line of credit is best used when:

• You want quick access to capital for unexpected opportunities or expenses.

• You’re scaling operations and need flexibility without long-term debt.

• You have seasonal cash flow fluctuations and need a buffer.

• Construction: Cover upfront project costs and manage cash flow between receivables.

• Wholesale & Distribution: Stock up on inventory before peak demand.

• Transportation & Logistics: Cover fuel, repairs, and fleet expansions.

• Manufacturing: Invest in equipment upgrades and raw materials without cash strain.

Ready to take the next step? Let’s get you funded.