Table of contents

Your business is raking in the wins lately, and suddenly you spot the perfect chance to scale fast. Maybe a competitor just went under and their prime retail space is available, or you've got the opportunity to acquire a smaller company that would double your market share overnight. You need cash, and you need it now, but your credit's solid and you're not about to tie up your equipment or property as collateral. That's exactly when an unsecured business loan comes in handy for seizing those make-or-break growth moments.

To make sure you’re always ready to capitalize on valuable growth opportunities, you should know what capital options you have available and which one is right for your company’s unique operations.

This guide will help you make that decision.

What is an unsecured business loan?

An unsecured business loan is a loan that doesn’t involve collateral. Collateral is a form of security for the lender in case the borrower fails to repay; typically, it includes real estate, equipment, and receivables, among others.

Unlike secured loans, lenders focus more on the company’s financials, such as its creditworthiness and historical revenue performance, as primary qualifications.

This is because unsecured loans are riskier than secured loans since they aren’t backed by collateral. Without collateral, the lender has nothing to recoup lost cost should the borrower default. As a result, unsecured financing typically comes with higher interest rates than secured loans or government-backed loans.

The growing market for unsecured business loans

Unsecured business loans are becoming an increasingly popular choice for companies looking to scale, especially those that prefer not to pledge collateral like property or equipment.

According to a recent Global Market Insights report, more than 70% of unsecured business loans in the U.S. go to small- to medium-sized businesses. This shows that smaller firms are embracing unsecured loans as a fast and flexible financing tool.

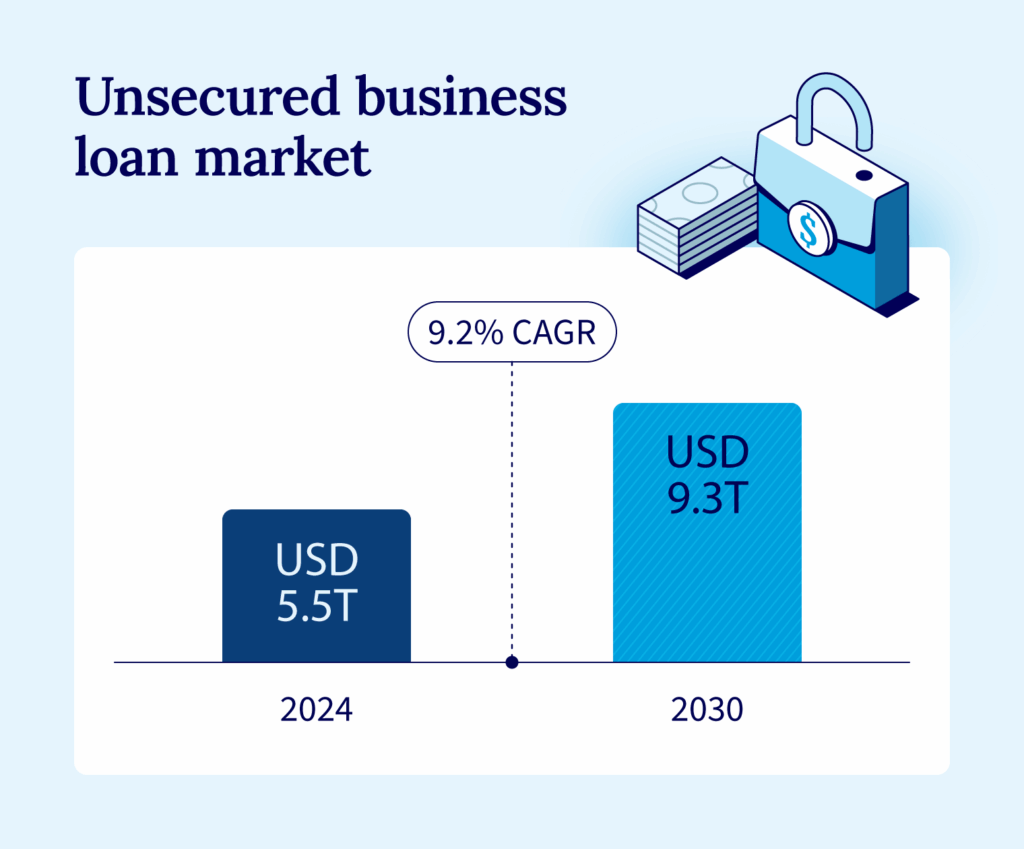

And the trend is only accelerating worldwide. The Research and Markets Unsecured Business Loans Global Strategic Business Report projects the total unsecured loan market will grow at a compound annual growth rate (CAGR) of 9.2%, reaching $9.3 trillion globally by 2030.

This market-wide growth indicates increasing lender confidence as well as high borrower demand, particularly from entrepreneurs prioritizing speed and flexibility over collateralized loan structures. For startups and expanding SMBs, unsecured loans are quickly becoming a mainstream financing strategy, not just a fallback option.

Best unsecured business loans at a glance

You’ve got plenty of capital options to choose from as you prepare for your next big move. Here’s an overview of the top lenders in the U.S.

| Lender | Max loan amount | Minimum credit score | Term length | Best for |

|---|---|---|---|---|

| National Business Capital | $15M | 620 | Up to 2 years | Flexible advisor-service |

| Bank of America | $250K | 700 | Up to 5 years | Long-term loans |

| U.S. Bank | $50K | Undisclosed | Up to 4 years | Fast funding |

| Wells Fargo | $150K | 680 | Up to 5 years | Lines of credit |

| OnDeck | $250K line of credit | 625 | Up to 2 years | Lower credit scores |

| Bluevine | $500K | 625 | Up to 2 years | Larger loan amounts |

| Fundbox | $250K | 600 | Up to 6 months | Short-term loans |

National Business Capital

Best for flexible advisor-service

- Max loan amount: $15M

- Minimum credit score: 620

- Term length: Up to 2 years

National Business Capital offers fast and flexible funding with some of the highest loan amounts in the industry, as much as $15M. The team is known for its quality service, with expert business advisors who work 1:1 with clients and assist throughout the funding process and afterward.

| Pros | Cons |

|---|---|

| Well-trained advisorsHigh loan amounts | Shorter loan termsHigher revenue requirements |

Bank of America

Best for long-term loans

- Max loan amount: $250K

- Minimum credit score: 700

- Term length: Up to 5 years

As one of the oldest banks in the U.S., Bank of America offers small loan amounts from $10K. However, the bank requires higher credit scores to receive funding, and its maximum loan amount is only $250K.

| Pros | Cons |

|---|---|

| • Term loans up to 5 years • Small loan amounts available | • Higher credit score requirements • Lower funding maximum |

U.S. Bank

Best for fast funding

- Max loan amount: $50K

- Minimum credit score: Undisclosed

- Term length: Up to 4 years

As one of the larger commercial banks in the country, U.S. Bank offers unsecured loans with funding amounts between $5K and $50K – lower than most competitors. However, they do offer fast funding through their “quick loan” option, which is available online.

| Pros | Cons |

|---|---|

| • “Quick loan” option available online • Funding amounts as low as $5K | • Doesn’t disclose credit score requirements • Low maximum loan amounts |

Wells Fargo

Best for lines of credit

- Max loan amount: $150K

- Minimum credit score: 680

- Term length: Up to 5 years

While Wells Fargo doesn’t offer unsecured term loans, it does provide unsecured lines of credit, which differ slightly from term loans. Although it has stricter credit requirements than other lenders, it does offer reasonable maximum funding limits and longer terms.

| Pros | Cons |

|---|---|

| • Longer repayment terms available • Includes rewards program | • Higher credit score requirements • Doesn’t offer term loans |

OnDeck

Best for lower credit scores

- Max loan amount: $250K

- Minimum credit score: 625

- Term length: Up to 2 years

OnDeck is an online lender that doesn’t offer unsecured term loans but provides an unsecured business line of credit, often funded the same day. The funding maximum for these lines of credit tends to be lower than that of other lenders.

| Pros | Cons |

|---|---|

| • Lower credit score requirements • Same-day funding for lines of credit | • Short repayment requirements • No unsecured term loan options |

Bluevine

Best for larger loan amounts

- Max loan amount: $500K

- Minimum credit score: 624

- Term length: Up to 2 years

Bluevine is a fintech company that provides banking solutions for small businesses, including business loans, through its network of lenders. The company offers some of the highest funding amounts available, along with lower credit score requirements.

| Pros | Cons |

|---|---|

| • High loan amounts available through lending partners • Lower credit score requirements | • Loans not offered through Bluevine • Terms and requirements can vary widely based on the lending partner |

Fundbox

Best for short-term loans

- Max loan amount: $250K

- Minimum credit score: 600

- Term length: Up to 6 months

Founded in 2013, Fundbox is fairly new in the small business loan industry. The lender has much less stringent requirements – three months in business with at least $30K in annual revenue and a 600 credit score. On the flip side, Fundbox has short repayment terms of up to six months.

| Pros | Cons |

|---|---|

| • Higher loan amounts • Ideal for startups and low-revenue businesses | • Extremely short repayment terms • Limited loan options |

Factors to consider when choosing an unsecured loan

As you’re reviewing unsecured loan options for your business, you’ll have a lot of variables to consider. Some of the most important factors to consider are:

- Interest rates: Unsecured loans come with higher interest rates since collateral isn’t involved.

- Repayment terms: Repayment can be as low as six months up to five years. While longer terms will decrease your monthly payment, you’ll also pay more interest over the loan term.

- Funding speed: Depending on the lender, you can access funds the same day,or it could take up to several weeks. Keep this in mind if you need capital quickly.

- Credit score: Lenders have different credit score requirements; some may require as low as 600, while others may need more stringent scores, like 700. Keep in mind that a lower credit score may bring higher interest rates with the loan terms.

- Lender reputation: It’s easy these days to research a lender’s reputation online, whether through Trustpilot, Better Business Bureau (BBB), or even Google Reviews.

Researching multiple financing types can help you better understand your capital accumulation needs.

How to get an unsecured business loan

You have several things to consider before applying for an unsecured business loan. Here’s a look at the general process:

- Consider the type of loan you need. Choose a term loan if you need a lump sum for a specific investment like equipment or expansion, as it provides predictable monthly payments. Opt for a business line of credit if you need flexible access to funds for ongoing expenses or seasonal cash flow gaps, since you only pay interest on what you use.

- Think about how much capital you’ll need. Borrowing too much can overextend your company financially, while borrowing too little may require you to submit another loan application. Approach this question strategically, and make the decision based on what’s best for your business and its goals.

- Check your credit. Credit score requirements can vary based on the lender, so you’ll need to clearly understand where you are before applying.

- Compare lenders. As mentioned, terms and requirements can vary widely based on your chosen lender. Do your research and choose a lender that makes sense for your business.

- Apply for your unsecured business loan. Once you’ve researched and have the right information, apply for your loan and be sure to ask any unanswered questions to a representative at your preferred lender.

Pros and cons of unsecured business loans

Any type of loan has its share of benefits and drawbacks, and unsecured loans are no different. Take time to weigh these pros and cons before applying for an unsecured loan.

| Pros | Cons |

|---|---|

| • No collateral involved means less risk • Faster funding because of the no-collateral process • Fixed payments • Lower interest rates than credit cards | • Higher interest rates than secured loans • Stricter eligibility requirements • Lower max loan amounts • Credit could be at risk |

Find the right unsecured loan with National Business Capital

Figuring out how to get a business loan isn’t always straightforward. The best lenders are financial planning partners that can help you assess your options and select one that best suits your goals. National Business Capital has years of experience helping clients find the right financing for their goals and has funded $3B+ for companies across America. Our team of expert business advisors will help you throughout the application process as you find the loan that best fits your business needs. Apply now to start and take your business growth to the next level.

ABOUT THE AUTHOR

Joseph Camberato is the CEO & Founder of National Business Capital, where he has led the company in funding more than $3 billion for growth-minded businesses since 2007. With firsthand experience building NBC from a startup into a national private lender, Joe writes on the economic forces shaping access to capital, including interest rate shifts, private credit trends, and the challenges mid-sized companies face when banks pull back.